[Two Cents #88] “Flights of Thought” on Consumer + AI — Part 14: Welcome to Clawverse! — Where the Consumer AI May Move to? (Part II)

Prelude

In [Two Cents #87 — Part I], we explored how the convergence of conversational AI and agentic code execution — embodied by architectures like OpenClaw — is producing something qualitatively new: an AI Concierge that can capture user intent, coordinate or create execution capabilities on the fly, and accumulate deep personalization over time. That was the what is happening.

In this Part II, I want to move from observation to projection. If a meaningful share of consumers adopts a real concierge agent — one that doesn’t just answer but operates — what changes in the structure of consumer software, distribution, and value capture? What existing profit pools get disrupted, and which new ones get created?

I’ll start with the structural framing that I believe matters most for understanding everything that follows (”The structure of the change ahead”), then will walk through three specific keywords — disruption of portals, app decomposition, device detachment, areas where the changes should be most consequential and where I’m focusing my investment attention. Then, the closing remarks on the future opportunity set for early‑stage founders and investors follows.

These are developing hypotheses, not declarations. My goal is not to fix a single “prediction” and defend it. It is to describe a set of structural forces shaping the surface on which the next generation of consumer AI products will be built—and to invite founders, operators, and fellow investors to refine or challenge these early theses.

I. The Structure of the Change Ahead

From “Attention Economy” to “Intent Economy”

As I discussed in [Two Cents #84], I believe there is a structural shift underway that deserves to be named clearly. For two decades, the consumer internet has operated on the logic of the Attention Economy. The entire ecosystem — Google Search, Facebook’s News Feed, TikTok’s algorithm, Amazon’s product rankings — was architected around a single fundamental constraint: we could never know exactly what a user wanted. We could only approximate it.

Website visits, clicks, dwell time, scroll depth, search keywords — all of these are “attention” signals that serve as the best available proxy for what the user actually intends to do. The entire $600B+ global digital advertising market, the SEO industry, the affiliate ecosystem — all of it was built on the logic of capturing eyeballs as an approximation of intent, then converting that approximated intent into economic value.

Hence, the “Attention Economy.”

AI changes this equation fundamentally. When a user tells an AI Assistant, “find me a family-friendly hotel in Kyoto for the first week of April, under $200 a night, with good vegetarian options nearby,” the assistant doesn’t need to approximate intent through click patterns. It has the intent — explicitly, precisely, in full context.

This is what I call the shift to the Intent Economy: AI-based environments introduce entities (ChatGPT, Claude, personal AI Assistants) that can explicitly capture user intent — not as a best approximation, but directly — and then execute on it. Cambridge researchers have described an emerging “intention economy” as a marketplace where human intentions become explicit commodities to be captured, interpreted, and acted upon in real time. Outlier Ventures calls it “a radical departure from our attention-centric internet,” where “platforms and services will now be designed to understand, interpret, and fulfill a user’s goals — often autonomously.”

This framing — Attention Economy → Intent Economy — is, I believe, the single most important lens for understanding every change I’ll describe below.

Who Captures Intent — and How?

If this framing is correct, then the most consequential question becomes: who captures the user’s intent, at what point, and through what mechanism?

Every major technology transition has been defined by the entity that seized the intent capture layer at the point of origin:

Web era: Search engines captured intent at the query box (Google → $2T+)

Mobile era: App stores captured intent at the download moment (Apple/Google)

Social era: Feed algorithms captured intent through engagement proxies (Facebook/TikTok → ~$1T each)

In each case, the entity that controlled distribution — the chokepoint through which intent flowed on its way to fulfillment — accumulated the most economic value.

In the AI era, intent is expressed directly through prompts, voice commands, and contextual instructions. Whoever becomes the default interface where that intent first lands will control the new distribution.

This leads me to a set of questions I keep returning to:

First, if everyone has an AI Assistant like OpenClaw handling their needs end-to-end, do we still need portals and gateways? Do we still need Google as a default starting point? Amazon as a default shopping destination? The honest answer, I think, is: increasingly less so.

Second, if the AI Assistant itself becomes the primary intent capture point, where does value concentrate? Probably in the Assistant and the Context/Personalization Memory it manages. But here’s the nuance: that value may be distributed across millions of individual assistants, each holding its own user’s context. There’s no natural aggregation mechanism — which could mean we end up with a multipolar equilibrium rather than a single winner-take-all structure.

Third, when an AI Assistant captures intent, where does it route the request? Directly to category-specific providers? Or through a new intermediary? And how does the assistant choose — user specification, bidding, marketplace dynamics, algorithmic optimization? The answers to these questions will define the new economics of consumer distribution. Whoever processes this routing step sits at the most strategic chokepoint in the entire new value chain.

Two Candidate Structures for Intent Capture

When I pressure-test the future, I see two competing structural candidates:

Candidate 1: The AI Super App remains the portal. An entity like ChatGPT, Gemini, or a new entrant becomes the dominant portal — a WeChat-like super app that captures intent as the default destination. This remains possible. It was my first conclusion on AI Super App, until OpenClaw architecture emerged.

But I’d argue the emergence of the OpenClaw architecture has significantly reduced this probability, at least in Western markets. The open, decentralized nature of the concierge model makes it harder for any single app to monopolize the intent capture layer. A new WeChat-style AI Super App emerging from scratch gets especially less likely now.

Siri and Alexa are interesting edge cases — they have the advantage of being embedded in hardware ecosystems (iPhone for Siri, Amazon’s environment for Alexa). But if those ecosystems themselves diminish in relevance as AI assistants become more capable and autonomous, Siri and Alexa’s claim to Super App status weakens proportionally. The smartphone’s role in consumer intent capture remains genuinely unsettled — and how it evolves will determine whether device-native assistants hold their ground.

Candidate 2: The AI Assistant becomes the primary concierge — and therefore the primary intent capture entity. I find this more probable given OpenClaw-type architectures. In this model, the user’s personal AI Assistant captures intent and then finds other entities — agents, services, providers — to fulfill it through machine-to-machine interaction.

The modes of fulfillment of ‘users’ intent’ will likely be diverse: search (advertising economics), recommendation (affiliate economics), marketplace (agent-to-agent negotiation), bidding (auction economics). Multiple modes will probably coexist across different verticals and use cases. The key insight is that intent capture distributes rather than centralizes — many assistants, each with a user’s context, rather than one portal aggregating all traffic.

The Timeline: “Gradually, Then Suddenly”

I don’t expect this transition to happen overnight. Over the next few years, existing portals and AI Assistants will coexist. Google will defend with AI Overviews, already appearing on 30%+ of queries. Amazon will push features like Buy for Me. But user behavior is already shifting — OpenClaw has garnered over 145,000 GitHub stars, and Baidu recently embedded OpenClaw-type agents into its search app for 700 million users.

Within 5 years, the roles and value distribution among major players will have materially settled. And over a 10-year horizon, the traditional portal model may resemble BlackBerry — structurally sound, but generationally obsolete.

This is a typical “gradually, then suddenly” pattern. Google, Amazon, Facebook, and Roblox each needed 10–15 years to reach their current dominant positions. As an early-stage investor, the 5–10 year window is precisely where the power-law opportunities emerge — betting on new structural players before the market consensus recognizes the shift as inevitable.

With this structural backdrop in mind, let’s turn to three specific keywords I’m watching.

II. Three Keywords — What Might Happen?

Keyword 1: Portal Disruption and Value Capture Restructuring

Background

The first and perhaps most provocative question: if everyone has an AI Assistant, do consumers still need the portals they default to today? Google for information. Amazon for shopping. The App Store for software. Facebook and TikTok for social content.

The answer, I think, varies by the type of service — and the nuance matters considerably.

Transactional services (search, shopping, booking, utilities) are the most directly threatened. When a user can express their intent to an AI Assistant and have it executed end-to-end — comparing flight prices, booking hotels, purchasing goods — there is simply less reason to visit Google or Amazon as a starting point. Intent capture migrates from the portal to the assistant. The portal’s “traffic concentration” role erodes.

Personal data-based services (email, calendar, document management) represent the classic “personal data + tool → app” bundle. In a decomposed world, the personal data migrates to a user-owned personalization layer, and the tool function becomes something an AI Assistant handles directly. The key issue here is personal data portability — and the degree to which users can extricate their data from existing platforms.

Externality-data services — where the product is the externality data itself — are more durable. Social networks live squarely in this category: the social graph and the interactions around it are inherently collective, not easily replicated by a single user’s AI assistant. But even here, social graph portability could erode the moat over time. If your social graph and interaction history become exportable, the switching cost of moving to a new experience approaches zero — and the moats of Facebook and Instagram become structurally weaker.

What Might Happen: Value Capture Restructuring

The structural implication: value migrates from centralized portals toward a distributed ecosystem centered on AI Assistants and the personalization data they manage.[1]

The new value concentration points will likely be:

The AI Assistant itself — as the primary entity interpreting and routing intent

The Context/Personalization data layer — the memory and preferences that make the assistant increasingly useful over time (what Scott Belsky calls “personalization effects” as the new network effects)

The Intent Routing layer — whoever intermediates the matching between user intent and service fulfillment

The players under the most direct pressure:

Google (search advertising ~$200B): the most directly threatened, with an estimated $130B+ in purchase-intent-related revenue exposed to migration

Amazon (search-based commerce): when AI agents begin to comparison-shop and purchase directly, the ~$55B in Amazon search advertising is at risk

The SEO industry: facing the most fundamental disruption in its history. Discovery mechanisms are changing at the root — zero-click rates already exceed 65%, and the shift from SEO to GEO (Generative Engine Optimization) is underway.

Existing Ad Networks: the foundational model shifts from Attention (impressions, clicks) to Intent (outcomes, fulfillment)

A few important caveats. I don’t think this collapses into a single new monopoly — particularly in the US market. The US consumer ecosystem is more fragmented than China’s. OS gatekeepers (Apple, Google, Microsoft) exert significant influence. Privacy and regulatory expectations are higher. The most likely outcome is a multipolar equilibrium: power-law outcomes within a multi-player structure rather than a single winner-take-all.

Underlying this entire restructuring is a question of state portability: can users take their data with them? Today, platform lock-in works because user state is trapped — your social graph in Instagram, your listening history in Spotify, your purchase patterns in Amazon. If Persistent State becomes separable (stored independently, exportable), then services can be re-implemented in real time by an AI Assistant using that state. The app stops being the locus of value; the state does. This is why DID (Decentralized Identity) and state portability infrastructure are not niche topics — they are the enabling technology for the entire value chain restructuring described above.

Investment Thesis Implications

Intent Routing Layer infrastructure: the new strategic chokepoint, regardless of which macro scenario prevails. The entity that intermediates between intent and fulfillment captures distribution-level value.

Personalization Infrastructure: personal data vaults, context stores, and state management protocols. “Personalization effects” replacing network effects as the primary retention driver.[8]

DID/Identity infrastructure: the next-generation “login” standard — a foundational layer that enables everything from state portability to social graph export.

GEO (Generative Engine Optimization): the successor to SEO — how services get discovered and selected by agents rather than humans.

Most at risk: businesses structurally dependent on portal traffic — SEO agencies, affiliate networks, display ad-dependent publishers. The $300B+ value pool in Google’s search advertising and Amazon’s commerce search alone represents the magnitude of what’s in motion.

Keyword 2: “Death of App”, or Rather, App Decomposition, then Reassembly as Intent Capture & Distribution

Background

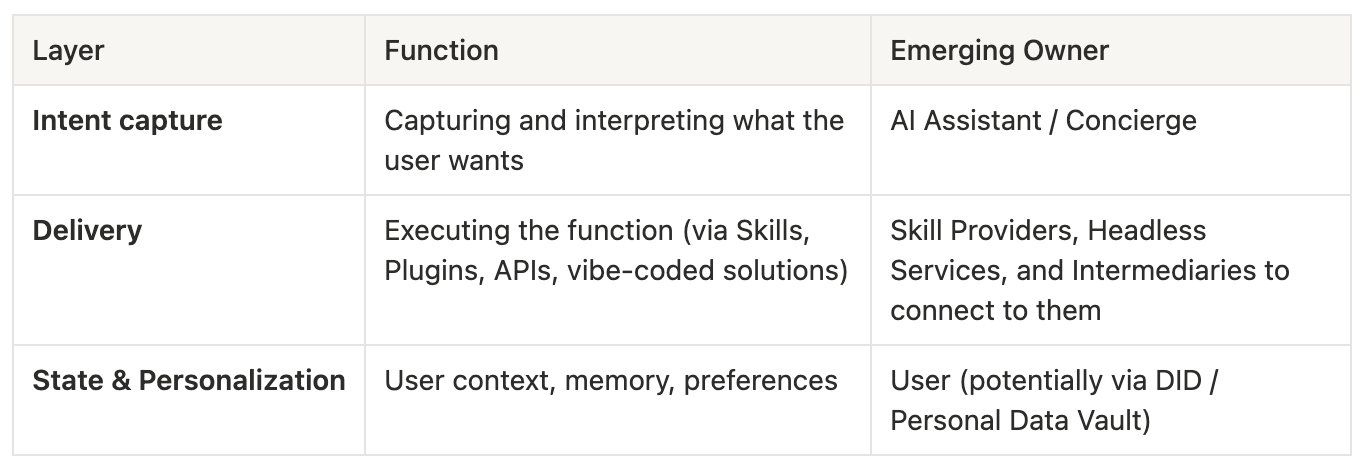

Today, an “app” is a bundled package: it captures your intent (through UI, search, navigation), delivers the function (features, integrations), and stores your personalization data (history, preferences, state) — all within a single unit.

In the Clawverse, this bundle breaks apart. An application decomposes into three independent layers:

In the old world, one app owned all three layers — and distribution was determined by two things: the app’s own delivery quality and the external discovery mechanism (Google search, App Store ranking). In the new world, each layer separates and can be owned by a different entity. The critical investment question becomes: which layer captures the most value?

My answer: the Intent Capture & Routing Layer. This is the new form of consumer app distribution — the AI-era equivalent of what Google Search and the App Store have been for the past two decades.

The precedent is consistent: in every technology transition, the entity that captured consumer intent at the point of origin accumulated the largest share of economic value. And the current market size at stake is staggering: Google’s advertising revenue (~$200B, of which roughly $130B relates to purchase intent), Amazon’s search-based advertising (~$55B), and App Store/Google Play revenue (~$200B). That’s a $400B+ market that gets structurally reorganized as intent migrates from search boxes and app stores to AI Assistants.

As Tom Tunguz has observed, the web is already flipping to agent-first design — “being findable” starts meaning “being usable by software acting for someone else,” not just ranking in human search.

What Might Happen: Three Directions for Delivery & Execution

The delivery layer — how user intent actually gets fulfilled — is where I see the most structural uncertainty. I expect a hybrid of three directions to coexist, with the relative weight of each still very much to be determined:

Direction 1: Direct routing. The AI Assistant identifies the optimal provider in each category and routes the request directly — essentially becoming an “AI Super App” that owns both intent capture and value accrual through its routing. If a new consumer platform emerges that hosts these assistants for mainstream users, it could function as a new kind of portal, reminiscent of the early web portal era.

Direction 2: Intermediated routing. A separate business may emerge to interpret and route intents — a new distribution layer analogous to what search was for the web and what app stores were for mobile. This is where I see the most interesting structural possibilities:

2-1: Single intermediary — one dominant router, like Google for search. Possible in theory, but I think unlikely to consolidate this way in the agent era.

2-2: Category-specific intermediaries — multiple routers, each serving a vertical. AI Assistants transact with these intermediaries through bidding or best-solution proposals. Value capture is distributed between the AI Assistant and multiple intermediaries. Google/Amazon-level concentration feels less likely; distributed value across numerous intermediaries feels more probable.

2-3: Headless providers — the AI Assistant, armed with personalization data, bypasses all intermediaries and goes directly to backend providers (e.g., for travel: bypassing Hotels.com and Kayak, going straight to GDS systems, hotel aggregators, local OTAs). Intermediary value capture vanishes almost entirely. This possibility was already demonstrated when GPT-4 placed orders directly with Instacart at launch. It will simply become widespread as AI assistants increasingly execute on users’ intent.

Direction 3: Direct execution via vibe coding. The AI Assistant doesn’t route at all — it builds the solution itself. Need a custom expense tracker? The assistant writes and runs the code. In this scenario, there is no third-party app capturing value whatsoever.

My expectation: Directions 1, 2, and 3 will all coexist in a hybrid structure. Direction 3 will handle simple, self-contained tasks. Direction 2 will handle complex, multi-party transactions. Direction 1 will emerge in verticals where a clear “best provider” exists. But the era of the app as a monolithic bundled unit is, I believe, structurally ending.

Investment Thesis Implications

AI Concierge Platforms: consumer-facing platforms that make OpenClaw-style AI Assistants accessible to mainstream users. Multiple are already appearing, though I’m skeptical any single one evolves into a dominant Yahoo!/Google-style portal. More likely: multiple coexisting platforms with power-law distribution.

Intent Routing / Marketplace Infrastructure (Directions 2-1, 2-2): the layer where agents find optimal services. I expect multiple mid-scale intermediaries rather than a single dominant player — more fragmented than today’s Google/Amazon duopoly, but still a collectively massive market.

Existing transaction infrastructure rewrite: SEO → GEO, Ad Networks → Agent Bidding, affiliate networks → agent-to-agent negotiation. This points to a market that could match the scale of today’s directly exposed advertising revenue ($400B+) or potentially the global advertising market (~$1.5T, roughly 1.5% of global GDP which is the US historical average of the gross ad market to the GDP).

Picks & Shovels: agent orchestration infrastructure, A2A (agent-to-agent) transaction rails — payment, trust, reputation, identity systems for the machine-to-machine economy. Tunguz predicts workers will manage ~50 agents daily; the coordination and transactional infrastructure this requires is a market unto itself.

Most threatened: standalone apps and single-function SaaS (decomposed into Plug-ins/Skills, heavily commoditized); App Stores (role shrinks from primary distribution to a single category of intermediary — a “Skill Store” with far lower value capture); and portal-dependent businesses whose discovery mechanisms are being fundamentally rewritten.

Keyword 3: Device Detachment and the New “Consumer OS”

Background

Today, your digital life is bound to your device. iPhone means Apple’s ecosystem. Android means Google’s. This coupling — hardware + OS + defaults + distribution — is the foundation of incumbent power. And the degree to which it persists or dissolves is perhaps the single most important variable determining who wins Consumer AI.

The logic is straightforward: as the AI Assistant becomes the user’s primary interface for expressing and executing intent, the need for specific apps, files, and desktops diminishes. If you don’t need specific apps, you don’t strictly need a specific device. This opens the possibility of device detachment — the user’s primary digital relationship shifting from a device to an AI Assistant that lives in the cloud.

In a device-bound scenario, the smartphone remains the default AI touchpoint. Apple’s devices would become the default AI Assistant provider — Siri evolves into Apple Intelligence, and Apple controls intent capture through OS-level integration, background execution permissions, and default settings.

In a device-detached scenario, the user’s personal AI Assistant becomes the primary interface — accessible from any screen, anywhere. The AI becomes the de facto “Consumer OS,” and the device becomes a commodity viewport.

OpenClaw is an early instantiation of this device-detached vision: chatbot conversation + vibe coding + agent execution happening through messaging apps and cloud interfaces, independent of any particular hardware or OS. This aligns with Belsky’s argument that “markets will be won or lost at the interface layer, and the ultimate interfaces are ULTIMATELY controlled by the operating systems of our lives” — except that in the AI era, the “operating system of our lives” may no longer be iOS or Android. It may be the AI Assistant itself.

What Might Happen: Three Options for the User-AI Interface

I think about this along a spectrum:

Option 1: Device-bound (status quo trajectory). Users keep personal devices (smartphone, forthcoming AR glasses) as the primary AI interface. Voice + screen UX. Apple’s current devices become the default AI Assistant provider. This is the most easily predictable scenario and the one incumbents are betting on.

Option 2: Voice-primary hybrid (most likely in the 5–10 year window). Voice becomes the main interaction modality; the smartphone screen is consulted only when needed for visual confirmation or complex decisions. This is the scenario I find most probable over the medium term. Its implications are significant: the role of both the device and the OS shrinks. The AI Assistant becomes the user’s primary touchpoint — what I’d call the de facto “Consumer OS.” User loyalty begins migrating from device brand to AI Assistant brand.

Option 3: Full device detachment (long-term possibility). No personal device required. A personal/ambient microphone for input. Any available screen for output. Identity-based access (most likely, DID) replaces device-based access. The user walks up to any screen, authenticates via identity, and their full AI environment loads. The device is a “viewer” — the intelligence and state live in the cloud.

If device detachment progresses, the user’s personal data stack may reorganize into distinct layers:

Layer 1 — Identity: who I am, portable and globally recognizable (DID). This becomes the access key that replaces device ownership.

Layer 2 — Personal State: my files (email, calendar, messages, social graph), my transaction history (shopping, payments), my preferences and context (the personalization layer).

Layer 3 — Dashboard: the real-time view of where my intents are being processed, their status and history. All my data on cloud/personal servers, accessible from any authenticated interface.

This is the dashboard-centric UX described in Part I — but with the critical addition that it is decoupled from any specific device or operating system.

Investment Thesis Implications

Two-school bet: Device-bound (Apple ecosystem remains dominant, AI integrated at the OS level) and Device-detached (third-party AI Assistants win the relationship). I’d maintain exposure to both, with increasing allocation toward device-detached as signals of voice-primary interaction and cloud-native AI dashboards accumulate.

“AI devices” — the new battleground: New form factors (AR/XR, ambient computing devices, wearables) where existing OS lock-in doesn’t apply. These represent greenfield territory — Meta’s AR explorations, startup hardware experiments, and the various “AI pin” attempts are all probing this space. As Belsky notes, “new approaches like Meta’s AR explorations” are emerging as alternatives to today’s reigning operating systems.

Ambient Computing infrastructure: the infrastructure enabling device-agnostic access — cloud-native dashboards, cross-device seamless experiences, ambient authentication, and the identity layer that makes it all work.

The key metric to watch: the ratio of AI Assistant usage time vs. native OS app usage time. When this ratio begins to tip decisively — when users spend more time in their AI Assistant than in traditional apps — the structural power shifts from device-maker to AI-provider. OpenClaw’s viral adoption through messaging apps (WhatsApp, Telegram, Signal) rather than through a dedicated native app is an early signal of this shift.

Closing Thoughts

These three keywords — Portal Disruption & Value Capture, App Decomposition & Reassembly, and Device Detachment & Consumer OS — are deeply interconnected and mutually reinforcing. Portal disruption creates space for new intent capture entities. App decomposition enables AI Assistants to assemble capabilities dynamically. Device detachment amplifies the AI Assistant’s role as the primary consumer interface. And identity/state portability is the enabling infrastructure that makes all of it possible.

I want to be honest about what I’m most uncertain about. The sequencing is unclear — does app decomposition drive device detachment, or vice versa? The speed is uncertain — will this take 5 years or 15? The market structure could go multiple ways — concentrated or distributed, platform-dominated or infrastructure-dominated.

What I feel more confident about is the direction. The value chain of consumer software is unbundling. Intent capture is becoming the new distribution. And the relationship between user and digital service is being mediated by an AI layer that barely existed two years ago. For an early-stage investor operating on a 5–10 year power-law horizon, the opportunity set here feels structurally as significant as the web-to-mobile transition — potentially more so, because it touches not just the application layer but the distribution, identity, and infrastructure layers simultaneously.

As mentioned earlier, these are developing hypotheses. I’d love to hear from founders building in these spaces, investors with competing frameworks, and anyone who spots the structural blind spots I’m surely missing.

The thinking gets sharper when it gets challenged.