[Two Cents #84] “Flights of Thought” on Consumer + AI — Part 10: Consumer Behavior Shifts — 2. The “Intent Economy” and the New “$1T Question”

Introduction

Human needs don’t fundamentally change. What changes is how those needs are served—the delivery mechanism, the form factor, the defaults, and the surrounding environment. When the delivery mechanism shifts, consumer behavior shifts with it—often gradually, then suddenly. And when consumer behavior rewires, business models and market structure follow.

There’s still debate about how large AI’s impact will be and where it will land. But in Consumer AI, the likely outcome isn’t just “the market gets a few times bigger.” The more consequential possibility is a structural rewrite: new consumer flows, new distribution, and a reallocation of value away from today’s incumbents.

This post is an attempt to map the shape of that business-model transition.

Where $1T of value capture is headed

As AI assistants—ChatGPT, Gemini, Claude, Perplexity (I’ll shorthand this whole class as “ChatGPT”)—cross the billion-user threshold, we’re starting to see early signals of a behavioral shift in how consumers use the internet.

When consumer behavior changes, business models change. And when business models change at internet scale, you’re not talking about a niche opportunity—you’re talking about new $1T outcomes (measured in terms of the market cap in the same league as Google and Amazon).

From “search” to “summary”

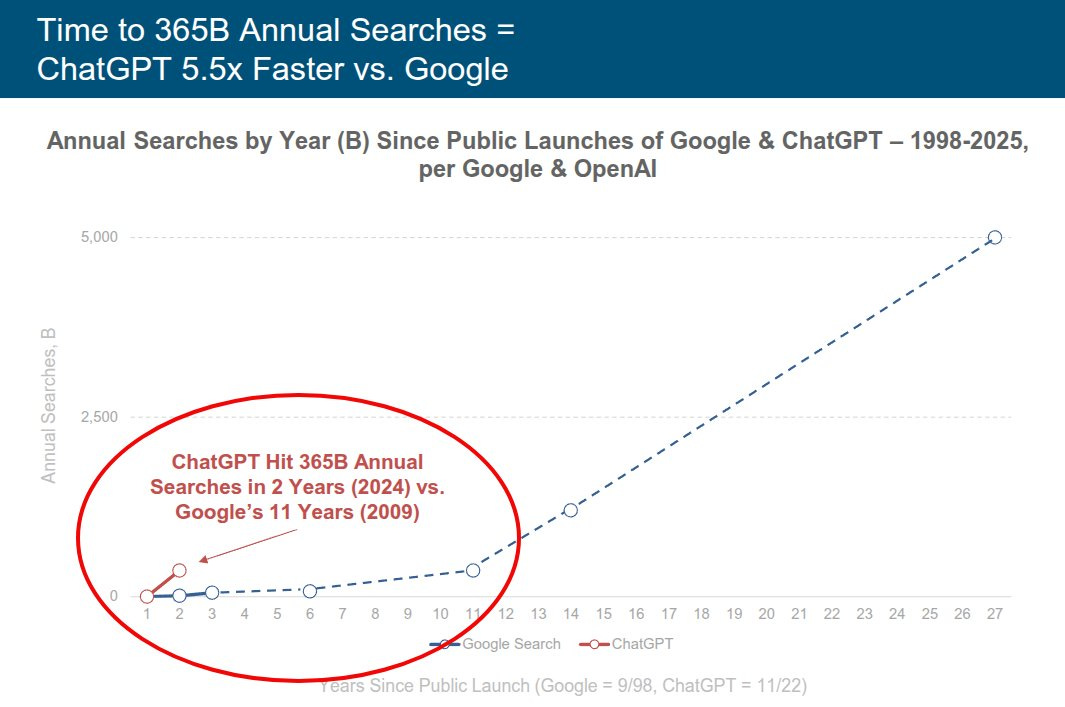

By 2025, estimates suggest that ChatGPT-driven query volume has reached ~10% of Google’s search query volume, and the “starting point” for information discovery is rapidly moving from Google to ChatGPT. Google took more than a decade to reach its current scale; ChatGPT reached comparable behavioral gravity in roughly two years.

More importantly, the function is shifting. AI assistants are moving from being a starting point (“search”) to becoming the endpoint (“summary”)—where users expect the answer directly, without needing to click out and browse.

That behavioral change matters because it reroutes the entire flow of traffic—what the internet has historically monetized as “attention.” The classic path was:

Google Search → SEO → ad networks → destination sites (commerce, services, news, info)

If the user journey increasingly ends inside an AI assistant, that traffic doesn’t follow the old route. And if traffic doesn’t follow the old route, revenue pools tied to that route become mobile.

If roughly ~50% of Google’s search traffic is “informational intent,” then a shift from search → summary implies that a meaningful portion of Google’s revenue is exposed. Against Google’s 2024 ad revenue base of roughly $265B (Search + YouTube + ad network), a back-of-the-envelope framing is that ~$130B of value may be vulnerable to redistribution into new channels.

The “purchase journey”: from “search & browse” to “intent & recommendation”

The same re-routing is happening for purchase-intent behavior—shopping, local, and professional services.

The first battleground is already visible: platforms are competing to own more of the purchase journey, and that competition is expanding beyond the boundaries of any single platform.

Historically, commerce platforms competed within their own walls: capture search, keep the user browsing, close at checkout. What’s changing now is that platforms are attempting to extend their control outward—effectively running search → browse → checkout on behalf of the user across other surfaces.

That dynamic is already creating friction between incumbents.

Amazon has pushed forward with “Buy for me”, where an agent handles discovery, comparison, and checkout from other platforms inside Amazon’s ecosystem.

In response, platforms are beginning to define new policy boundaries around agent access to product data and checkout—with examples like Amazon restricting agent access entirely, and Shopify allowing access to product pages while limiting checkout pathways.

The next step is the AI assistant itself absorbing the full purchase flow. OpenAI’s “Instant Checkout” directionally signals a future where a user can complete search, browse, and checkout without leaving ChatGPT. That’s the start of a new competitive frontier: ChatGPT vs. commerce platforms for ownership of the consumer purchase journey.

If you broaden the lens, this goes beyond buying a single item. AI assistants are increasingly providing “full-stack intent fulfillment” for multi-step tasks that require planning, research, and curation—e.g., “Plan a trip to X with Y budget”—including vendor discovery and evaluation.

This is exactly the experience commerce and booking services have wanted for decades, but couldn’t deliver due to technical constraints.

And these behaviors are no longer hypothetical.

In my own case, when my family planned an overseas trip in summer 2025, an in-chat agent (specifically Manus in this case) did the research: proposed an itinerary, surfaced hotels, and identified local travel agencies. We then completed bookings through the relevant providers—but critically, we did not need Google search at any point for planning or discovery.

Full agent execution—booking the hotel end-to-end, negotiating with a local operator via voice and messenger, etc.—is not universally productized yet. But the components are already real:

hotel booking automation is already feasible in agentic workflows

outbound/inbound calls via AI have been demonstrated for years (Google’s Duplex demo in 2018 was the early proof point), and AI-assisted calling is increasingly normal in specific verticals (reservations, outbound sales), at least in the US market

What’s still missing is not capability—it’s packaging, incentives, and rails (including the affiliate layer that routes demand to sellers in a way sellers will accept).

At a technical level, agents can execute the entire transaction pipeline:

for ecommerce: search → SEO → ecommerce front-end → product page → checkout

for service providers: affiliate network → service provider → checkout

Which implies a deeper substitution: search → browse → checkout gets replaced by task → recommendations → selection.

When that happens, traffic—and therefore monetization—no longer needs to flow through Google, ad networks, affiliate networks, or merchant/service-provider front-ends. The value capture shifts upstream to wherever intent is interpreted, executed, and monetized.

Considering roughly 50% of Google’s traffic carries purchase intent, ~$130B of Google revenue is in the blast radius. And Amazon’s ~$55B annual search advertising revenue is directly exposed as well.

“Attention Economy” → “Intent Economy”

The Intent Economy

The cleanest framing is that the internet is reorganizing from an “attention-first” system to an “intent-first” system.

The Attention Economy was built around approximating intent indirectly—through traffic patterns and engagement signals. The primitives looked like this:

user arrives (eyeballs)

the system infers intent from signals (queries, dwell time, likes/comments)

the system optimizes response to drive reaction (click)

the user browses tools/interfaces toward decision (conversion)

revenue accrues to the destination and intermediaries (sales/subscription/ads)

User flow: eyeballs → attention → click → conversion → revenue / gross margin

If you reverse it from the money side (simplified for commerce):

merchant generates ~30% gross margin

~half of that (10–15% of the purchase price) goes to sales/marketing/brand spend

that spend gets allocated across branding, performance marketing, affiliate, ad networks

and ultimately lands with platforms like Google, Meta, TikTok/Instagram, Amazon, and media pages

Value accrual: GM (30%) → marketing budget (10–15%) → affiliate/ad layers (~5%) → platforms

This entire architecture of Attention Economy in the current system exists because true intent was hard to grasp, so the industry got very good at modeling it from proxies: CTR, conversion funnels, A/B testing, attribution.

The Intent Economy flips the order.

If the system can capture intent directly (through prompts, context, or memory inside the AI Assistants) and execute the exploration process on the user’s behalf, then the core loop becomes:

understand intent

run search/browse/analysis through agents

deliver the best matched recommendation

execute (with or without human approval)

A simplified future state would be like:

User flow: intent/context → “concierge agent” → multi-agent swarm → delivery (product/service/content)

Value accrual: GM (30%) → brand/marketing/sales agent → recommendation agent → intermediary agent swarm → “concierge agent” → delivered to user

This isn’t a solid structure yet. It’s highly fluid, and multiple versions will be tested in the market. Even if stabilization takes a decade+, we should expect intense competition over the next 2–3 years, and the beginnings of a durable role/value map within ~5 years—similar to how Web 1.0 markets formed and consolidated.

Note on the “concierge agent”

The concierge agent is the layer that owns the user relationship and orchestrates intent fulfillment. Long-term, it likely becomes the most important choke point for value capture—especially once it is powered by a real personalization layer (agent form factor vs. data layer form factor remains unclear). The current “AI Super App” race is, at its core, a race to own this layer. I’ll cover that separately.

How the intent flow changes across the funnel

The simplest description: from “user-driven exploration” to “agent-driven delivery and execution.”

In the Attention Economy, the consumer journey is typically framed as: Discovery → Engagement → Conversion → Loyalty/Retention

Mapped to the Intent Economy, each stage changes meaning as follows:

I. Discovery

In the Attention Economy, discovery is about capturing attention through search, SEO, ads, content, and branding.

In the Intent Economy, discovery becomes: understanding intent and initiating execution.

fades: attention capture (search/SEO), affiliate marketing, ads, social discovery

emerges: intent interpretation, personalization, transaction initiation, agent competition/swarming, results comparison, personalized selection

Core components:

Concierge agent: interprets intent, triggers transactions, routes results, requests approval (human-in-the-loop) or executes autonomously

Personalization layer: filters/selects outputs based on user context (embedded in the agent or accessed as a data layer)

Infra: delegation permissions, rights management, privacy

II. Engagement

In the Attention Economy, engagement is about keeping users in the funnel: UX optimization, reviews/social proof, recommendations, metrics.

In the Intent Economy, the focus shifts from engagement to delivery: agent negotiation, execution, and verifiable outputs.

fades: UI personalization as funnel optimization, A/B testing for clicks, review-driven persuasion as primary tool

emerges: agent-to-agent negotiation, machine-readable execution artifacts, micro-transactions/financial rails for agent commerce

III. Conversion

In the Attention Economy, conversion is optimized through checkout design, cart recovery, upsell/cross-sell.

In the Intent Economy, conversion becomes: execution + closing—either via human approval or direct agent action.

fades: checkout-flow optimization, cart abandonment tactics, upsell/cross-sell mechanics

emerges: human-in-the-loop confirmation, direct agent execution, payment rails designed for agent finalization

IV. Loyalty & retention

In the Attention Economy, loyalty is maintained through branding, loyalty programs, retargeting, and repeated re-entry into discovery/engagement loops.

In the Intent Economy (outside of certain categories like luxury), loyalty mechanics likely weaken. Branding and loyalty won’t disappear, but their marginal impact should compress because the system optimizes for intent-match delivery, not for attention capture.

fades: branding as primary retention lever, loyalty programs, retargeting

emerges: continuous competition over intent outcomes; new strategies to influence the personalization layer

What changes should we expect?

Much of this remains speculative. But directionally:

A rewrite of B2C infrastructure: SEO, ad networks, affiliate networks, creator-economy tooling

The roles may not vanish, but the value propositions and handoffs across the chain will change.

Current incumbents likely might have a ~5-year window to adapt; growth-stage players must either start natively in the new structure or continuously re-architect in real time.

Commerce likely would change first and most violently. It’s where intent is easiest to monetize and where the funnel is most directly measurable.

**Marketplaces will be rebuilt. “**Discovery and connection” mechanics are changing at the protocol level. The next-generation marketplace likely won’t look like the current one—even if much current commentary focuses on how incumbents defend today’s structure rather than imagining a new one.

Key takeaways

The core implication is simple: many assumptions that shaped internet playbooks for the past 10–30 years are no longer stable. Business models built on those assumptions may become obsolete faster than people expect.

There’s a recurring failure mode in tech transitions: even after a new paradigm arrives, old business models keep growing due to inertia, which leads people to underweight the probability of structural change.

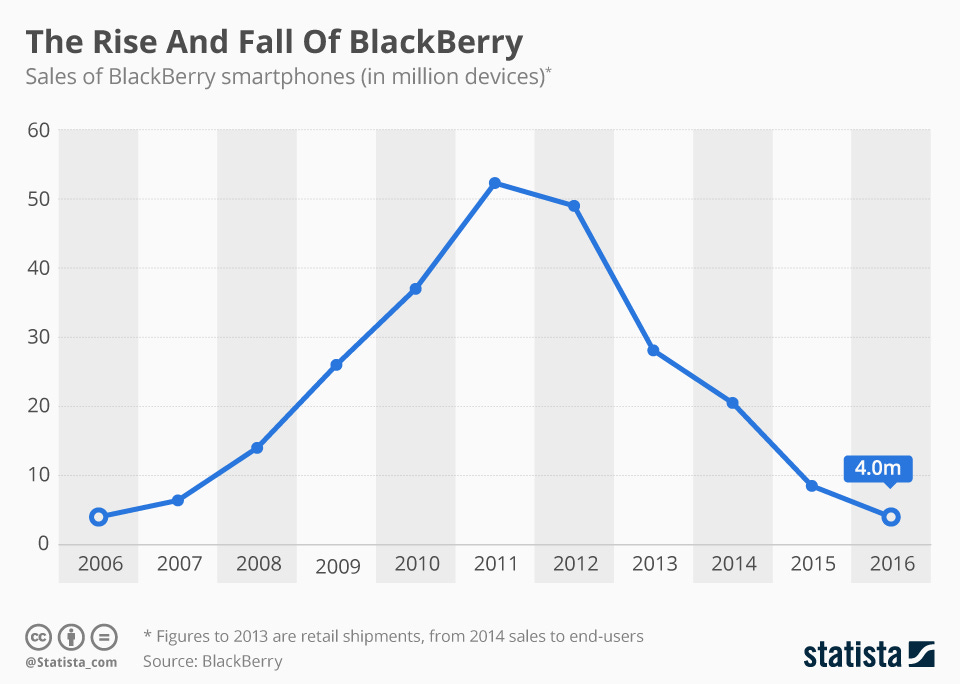

BlackBerry is a clean example. In retrospect, its collapse looks inevitable after the iPhone. But historically, BlackBerry actually grew for years after the iPhone (2008) and App Store (2009). It peaked around 2011—roughly 4x larger than it was in 2008.

The lesson: a business can be growing—strongly—while still moving in the wrong direction relative to the next market structure. And a decade later, it becomes the new BlackBerry.

If you’re building now, don’t be the “BlackBerry” of the Intent Economy.