[Two Cents #85] “Flights of Thought” on Consumer + AI — Part 11: Consumer Behavior Shifts — 3. From “Interface” to “Intent”

Prelude

Human needs don’t fundamentally change. What changes is how those needs are served—the delivery mechanism, the form factor, the defaults, and the surrounding environment. When the delivery mechanism shifts, consumer behavior shifts with it—often gradually, then suddenly. And when consumer behavior rewires, business models and market structure follow.

There’s still debate about how large AI’s impact will be and where it will land. But in Consumer AI, the likely outcome isn’t just “the market gets a few times bigger.” The more consequential possibility is a structural rewrite: new consumer flows, new distribution, and a reallocation of value away from today’s incumbents.

In [Two Cents #84], I looked top-down—how the value chain is being reassembled and what that implies for market structure. Here, I’ll go bottom-up: what becomes newly possible because of AI, what new consumer behaviors emerge, and what second-order effects those behaviors create.

I. “YouTube-ification of Everything”

The first pattern worth naming is what I’ll call the “YouTube-ification of everything.”

By “YouTube-ification,” I mean this: tasks that used to be inaccessible to everyday users—because they required expertise, time, tooling, or scarce resources—become broadly doable thanks to a new technology. Over time, that creates entirely new consumer behaviors, not just new features.

YouTube’s 2005 breakthrough wasn’t simply “online video exists.” It was the removal of friction: digitize, upload, and instantly watch without wrestling with formats, codecs, or downloads. Once watching and sharing became trivial, video consumption and distribution commoditized—and an entire behavioral and economic layer emerged on top of that. “YouTube-ification” is that broader phenomenon: a technology makes something newly possible at scale, and the behavior that follows becomes mainstream.

AI-driven YouTube-ification is already showing up across more domains than most people expected—and it’s spreading fast.

It started with image and video generation, which was the first “wow” moment for the mainstream. But it quickly expanded to music, 3D model generation, 3D animation, and now even real-time 3D world models you can navigate. (Examples: Google Genie3, World Labs.)

And it’s not limited to “creative content.” If you zoom out, “vibe coding” is part of the same arc: making software creation accessible to non-experts. At the extreme end, you now see platforms that turn software building into a social activity—closer to writing and sharing than traditional development (Wabi)—and even game creation via vibe coding (Verse8).

If everything—from images and video to games and software—gets YouTube-ified, what happens to consumer behavior? Even if you restrict the thought experiment to “content creation,” the scale feels not 2–3x, but 100–1,000x relative to prior creative revolutions (think the invention of the camera). And at that scale, you don’t just get more volume—you get qualitative behavioral shifts.

A few plausible first-order and second-order effects:

Professional content moves upmarket toward stronger narrative and higher production quality

Similar to how photography pushed painting into new forms and branches.

Consumer-generated content becomes less about the artifact, more about the behavior around it

Snapchat: disappearing media enabled deeply personal, conversation-native social behavior.

Early TikTok: “music video battles” mattered less as content and more as social interaction.

Real-time, personalized generation and navigation of 3D models / virtual worlds / games

AI-assisted “spatialization” as a new default—raising the question: what new behaviors emerge in AI-shaped spaces?

Commoditized software creation → software as a utility (more below)

What other second-order behaviors become possible once these first-order shifts go mainstream?

Note: The examples above mostly stay at the first-order level. That’s a limitation of imagination, not importance. If first-order shifts create near-term opportunities, second-order shifts are often the next wave—likely emerging 2–3 years later, built on top of the first.

Software as a Utility

The most extreme expression of this worldview is something I say informally: software becomes a utility—like electricity or water.

Today we take electricity for granted: plug in anywhere and it works. But if you look at the early history of electrification—even just ~100 years ago—using electricity in a neighborhood required custom wiring, local generation, and bespoke infrastructure shaped by building layouts and density. The transition to modern electricity—standardized voltage, national-scale distribution, metering, and “plug-and-play” access—required decades of technical standardization, industry consolidation, and infrastructure consolidation, catalyzed by leaders like Samuel Insull.

Software’s evolution since commercial adoption in the 1960s is structurally similar:

Hardware- and task-specific programs (ENIAC, Apollo 11-era code) → vendor-led hardware standardization (IBM) → OS/platform consolidation by hardware scale (IBM, DEC) → off-the-shelf OS standardization (Unix, Microsoft) → shrink-wrapped software → client-server → cloud/SaaS → vibe coding → and eventually, software as a utility (still ahead of us).

If you buy this arc, the next phase is “software as utility,” or the mainstreaming of “one-time-use software.” Vibe coding is an early signal. Platforms like Wabi - built around sharing vibe-coded software - look like the beginning of “software’s YouTube moment.”

A few plausible behavioral implications (again, mostly first-order):

First, we may stop thinking of software as an “object you build” and start treating it as a disposable “tool you summon” to accomplish a job. As tools are created and shared—and as remixing becomes normal regardless of whether the output looks like an app, a SaaS endpoint, or an agent

The first consumer behavior shift is straightforward:

people will try to find tools before they try to build them. This resembles early “GPTs” or today’s prompt libraries, but likely becomes far more consumer-native.

If that happens, the place where people browse, buy, and exchange tools may look less like an App Store or Zapier-style marketplace, and more like a consumer retail experience—think Amazon or Coupang, optimized for discovery, trust, and conversion rather than developer packaging.

A second behavior is also likely: rent-and-discard becomes normal—using software once, then moving on.

Over time, the “tool-sharing” space could evolve beyond tools into an arena for best practices, workflows, and mental models—ultimately becoming a social commons for “how to work” and “how to live.” Instagram didn’t stay a “pretty photo app”; it turned into identity, then marketing, then commerce. A tool commons could follow a similar path.

Second, as software fades into the background, consumer attention shifts from tools to workflows.

Many of today’s habits—email, calendars, to-do lists—aren’t “natural”; they’re behaviors shaped by the tools that existed (not the other way around).

If tools become as abundant and disposable as electricity, “using a tool” stops being a conscious act. The focus moves to what you’re trying to accomplish with the tool—like cleaning a room or watching TV, not “using electricity.”

The analogy is the internet itself: it used to be a high-friction activity (“doing the internet”); now it’s ambient.

What additional second-order behaviors emerge once this becomes a default?

AI Scientist

This isn’t directly consumer behavior, but if you extend the “YouTube-ification” thought experiment to its logical endpoint, one destination is frontier R&D.

One of the most interesting AI-native categories emerging at the SOTA frontier is “AI scientists.”

About a year ago, there were announcements of agent-only research teams discovering new Covid-19 vaccine candidates without human intervention. Now, teams composed primarily of AI agents are becoming more common. It’s plausible that “vibe coding for science” becomes real—at least for professional researchers—sooner than we think.

As foundation models improve, the bottleneck shifts from raw modeling to domain knowledge and problem framing. That suggests the first breakout domain could be drug discovery and life sciences, where value-add is enormous and the data/constraints are deeply technical. We’re already seeing “AI scientists” emerge in life science in a way that resembles early startup formation.

Push that far enough, and you can at least entertain a bigger question: could this be the practical starting point for an AGI/ASI-driven “intelligence explosion” that many visionaries speculate about?

II. “No App, No OS” — The End of UI/UX as We Know It

If “YouTube-ification of everything” is the first shock, the second is what it implies about interfaces.

Two implications stand out:

The abstractions we’ve taken for granted—OS, software, apps—and the businesses built around them may be dismantled and recomposed.

The resulting consumer behavior shift could be far larger than we’re currently modeling.

“AI is being baked into keyboards, browsers, and operating systems. If your assistant is everywhere you type, why open a separate app?” — 2025: The State of Consumer AI | Menlo Ventures

Elon Musk recently claimed that within 5–6 years, OS and apps will become unnecessary; users will talk to an AI-enabled device (likely not a smartphone), and most content people see will be generated in real time as needed.

Musk is often controversial, but his first-principles instincts—setting a direction, then building toward it—are hard to dismiss. I’m not sure about his exact timeline, but I think the direction is broadly right: the concept of “software” and the way humans interact with it—including the OS layer—may change at a foundational level.

It’s also worth remembering how young the “mobile app” artifact really is: ~20 years since modern smartphones, perhaps 30–40 if you go back to Palm Pilot-era apps. Apps exist because the smartphone existed. If the smartphone itself becomes less central over the next few decades, it would be odd to assume the “app” remains the dominant interface primitive.

One useful framing: “This multiplayer AI moment will create entire categories of software we don’t have names for yet, because the structure of collaboration is about to change from ‘people using apps’ to ‘groups interacting with intelligence’” — Greg Isenberg on X

The UI/UX Reset: From Interface-Heavy to Intent-Driven

This transition implies a deep reset in how humans and systems connect—both at the UI touchpoint and across the broader user experience.

As discussed in [Two Cents #76] UI, UX, the interface layer is likely to change along several dimensions. This won’t fully happen in the next three years, but it also doesn’t feel like a 10+ year story.

1) The end of “request–response UX”

The most fundamental shift is the decline of the classic loop: the user requests something through a UI, the system responds, the user requests the next step, and so on. That interaction model will be replaced in multiple ways.

Consider an ambient agent that proactively intervenes. Instead of waking up and scanning email and calendar, a 24/7 assistant summarizes your day over breakfast: priorities, context, trade-offs, and suggested actions—then asks lightweight questions like “Should I proceed?” If users get comfortable with this, why would anyone care which email client, calendar app, or to-do list product they use?

2) Where is the primary UI surface?

If intent becomes the primitive, what becomes the default surface? The smartphone again? The desktop? Or ambient environments—cars, offices, homes, public transit, streets—filled with cameras, microphones, and speakers? Or new form factors like pins, AR glasses, or wrist-worn devices?

3) What is the primary interaction modality?

Is it still screen-first—typing and uploading—just with smarter AI? Or voice as the default? If voice, who is the counterpart: Siri-like assistants, ambient devices like Alexa, or a dedicated AI app? If the interaction is ambient, does a cloud agent triage continuously?

4) Who becomes the primary interaction “owner” before the new world arrives?

During the transition, what becomes the primary orchestrator in today’s device environment? Does Siri become the front door and route everything else? Do ChatGPT/Claude become a new super-app—and effectively a new app store? Do users navigate “AI URLs” or standalone AI apps like they do today? Or does the browser reassert itself?

In aggregate, this points to a behavioral shift: consumers move from interface-heavy UI/UX to intent-driven workflows.

Some near- and mid-term implications:

In the short term, the platform-based web/app environment begins to fragment, and apps/services/mini apps reorganize around new platform layers.

Early signals include the OpenAI App SDK and Apple’s newly announced Mini Apps Partners Program. (My related notes posted on X: App SDK, Apple Mini Apps.)

The “new platform layer” could settle at iOS/App Store, an AI browser, ChatGPT (an “AI super app”), or a distributed mix. Where it lands depends on technical trajectories and consumer adoption.

Combined with “software as a utility”—and the broader idea that “SaaS is dead, at least as we know it” (a topic for later)—the market may simultaneously:

aggregate into a smaller number of headless suppliers, and

fragment into an ecosystem of countless micro/mini apps (often single-purpose), reminiscent of mini programs inside WeChat.

This reconfiguration will reshape the front-end interface layer and the back-end headless supplier layer—likely over a long time horizon (10+ years).

Travel is a concrete example. Today’s structure is dominated by consumer-facing aggregators like Booking.com and Hotels.com. A plausible future structure is: an AI super app or agent becomes the consumer-facing front-end, while a small set of headless booking suppliers—air (GDS like APOLLO, AMADEUS) and hotels—become the back-end infrastructure.

III. Second-Order Effects on Consumer Behavior Shifts

Once AI moves beyond “automation for efficiency” and “content generation” into agent-led judgment and execution, the basic unit of consumer behavior stops being apps, pages, or features. Users begin with intent (“what am I trying to accomplish?”), and the system handles search, comparison, execution, and follow-through as one continuous flow.

This is less a UI/UX evolution and more a shift in how consumers conceptualize digital systems.

Reframed as second-order behavioral changes:

Mass creation: consumers don’t just consume outputs—they consume participation

The most direct consequence of “YouTube-ification” is that creation is no longer reserved for experts. As the cost of producing images, video, music, 3D, code, and games collapses, consumers naturally move across the boundary between producer and consumer. The key isn’t that outputs get better; it’s that making becomes normal.

The second-order effect is a shift in attention. Consumers increasingly value the live-ness of the process, the ability to participate, and the social context of remix and feedback more than the finished artifact. As with early TikTok battles or Snapchat’s disappearing media, the “work” isn’t the point—the relationships and interactions around the work are. Consumers act less like audiences and more like co-creators and curators.

And this isn’t limited to media. Software itself is becoming a consumer creation surface, and platforms like Wabi are early examples of consumer-native creation and sharing around vibe-coded software.

The end of search and browsing: “finding” fades; “delegating” becomes default

A large fraction of the legacy internet was built on search and exploration. To solve a problem, you formed queries, opened links, compared pages, and made decisions yourself. As AI replaces that workflow (search → summary), consumers stop gathering information and instead provide constraints and decision criteria—then accept or reject the system’s output.

That’s a subtle but foundational change. Cognitive load moves from “how much did I read?” to “how much do I trust this system?” The important question becomes not what was chosen, but why it was chosen—and whether that choice is reversible. The end of search UX is not just the disappearance of a search box; it’s the transition from exploration-first thinking to intent-first thinking.

Software as a utility: consumers don’t “use tools”—they accomplish work

When software behaves like a utility (electricity/water), consumers stop thinking of themselves as “people who use tools.” Much like we no longer say “I’m using the internet,” the act of using software becomes invisible. In a world where capabilities are summoned on demand and vanish when the job is done, installing and learning apps becomes the exception.

As a result, behavior reorganizes around workflows. The focus is no longer which email client, calendar, or to-do app you use, but how you run your day and how you sequence tasks. Software stops being an identity or productivity object and becomes background infrastructure—sometimes visible, often not—that enables outcomes.

The collapse of request–response UX: users don’t operate systems—they approve flows

Traditional UI/UX is built on a repetitive request–response loop. But when agents maintain context and take responsibility for end-to-end workflows, that loop weakens. Users stop asking “what should I click?” and start approving, rejecting, or adjusting the system’s proposed plan.

In that world, UX is less about interface complexity and more about the design of intent transmission and decision processes—delegation, human-in-the-loop checkpoints, frequency of intervention, escalation rules, and personalization. “Good UX” becomes: ask the minimum number of questions at the right moments, and help the user decide—or decide on their behalf within clearly defined bounds.

The core “cost” of consumption shifts: from money to intent, trust, and permission

Finally, the nature of what consumers “pay” changes. As time and attention spent inside apps declines, users delegate more to systems. The scarce resource becomes not dollars, but trust—and the permission to act.

In that context, ad-driven feeds and click-optimized funnels weaken. Consumers express intent; agentic systems focus on delivery. The economy shifts from what I described in [Two Cents #84] as the “Attention Economy” toward an “Intent Economy.”

Premium value accrues not to content, clicks, or conversion mechanics, but to the quality of delegation: how confidently a consumer can trust the system, how decisions are made (HITL, delegation), and how failures are audited, explained, and reversed. Consumers will do less themselves and delegate more—and the design of that delegation will define the next generation of consumer experience.

IV. Market Structure Shifts and New Startup Opportunities

Market structure: from “app-centric internet” to “agent-centric economy”

As AI takes ownership not only of generation but execution, the foundational unit of the consumer internet moves from apps to intent. Instead of searching for functionality, installing software, and learning workflows, users state goals (explicitly or implicitly) and rely on systems to decompose and orchestrate actions. Value accrues less to UI polish or feature breadth and more to who can correctly interpret intent, delegate execution effectively, and design the decision boundary: who decides what, and how.

In practice, the “driver” of this process is less the human user and more a multi-level swarm of agents coordinating tasks. The service providers behind the scenes increasingly appear as headless infrastructure—agents, micro-services, and capability endpoints—rather than consumer-facing apps.

This naturally polarizes the market. On one end, standardized supply consolidates into a small number of headless suppliers/aggregators (travel is the canonical example via GDS). On the other end, micro-capabilities explode: skills, mini apps, tools, single-purpose endpoints. Where “big apps with many features” once dominated, we shift toward workflows that dynamically call whatever capability is needed. The user experience is no longer defined by cross-app switching costs, but by end-to-end “intent → execution” quality.

Player reconfiguration: where does the new platform live?

In this world, “platform” is no longer primarily about app distribution (like an app store). It’s about being the first surface where intent is expressed. Layers that sit at the everyday gateways—keyboard, browser, OS, notifications, payments, identity, contacts, calendar—have the most natural access to user context and permissions. That positions them to evolve from “hosting apps” to routing intent: deciding which model, service, or API to call, when. As the act of opening apps declines, that layer becomes the real distribution channel.

At the same time, AI super apps (ChatGPT-like) or AI browsers can become the new portal—except the portal no longer routes to links; it completes tasks. The competitive moat shifts from response quality to orchestration reliability: persistent understanding of user context, stable integration across external tools/suppliers, and the ability to reverse outcomes when something goes wrong (control, auditability, guarantees). This becomes less a fight over “who owns the app ecosystem” and more a fight over “who owns permissions + context,” and therefore who controls execution flow.

Startup opportunities: not “another app,” but a better execution layer for intent

The largest opportunity here is not building yet another app, but building the layer that executes intent better. Most real-world goals are multi-step and constraint-heavy (e.g., “optimize a family trip to Jeju this weekend”). Products that can decompose intent, connect data and tools, validate outputs, and handle exceptions will win. The product isn’t UI. The product is progress.

A second major opportunity is the trust and permission layer—delegation by design. When AI can pay, book, message, and submit documents, consumers don’t want more eloquent answers. They want accountability: who is responsible when it’s wrong, what evidence drove the decision, how far permissions extend, and how quickly delegation can be revoked. That creates demand for provenance, audit logs, policy-based permissions, rollback mechanisms, and even guarantees/insurance-like constructs. This is not “feature work”; it’s foundational infrastructure that makes delegation psychologically safe.

Finally, as capabilities atomize, the market converges on discovery and composition. Consumers won’t browse endless micro tools. They will expect systems to curate and bundle capabilities around goals. The resulting opportunity looks less like “App Store 2.0” and more like workflow-native commerce and distribution. Examples that feel natural in this direction:

Goal-based packaging: input “interview prep,” “moving,” or “kid’s birthday party,” and get tools, content, checklists, and execution bundled end-to-end

Agent-native commerce infrastructure: standardized product/service metadata, real-time price/inventory/policy APIs, and automated post-purchase customer support

Personal data vaults: secure storage of personal context (calendar, relationships, preferences, finances) with policy-based partial delegation to agents as a personalization layer

In short, the weakening of the app-centric ecosystem doesn’t mean “products disappear.” It means the center of gravity shifts toward intent execution flows and trust-by-design systems. In this transition, the most promising wedge points are: (1) intent routing and orchestration, (2) trust/permission layers, and (3) distribution, bundling, and discoverability for micro-capabilities—areas where new tier-one consumer and platform companies can emerge.

Key takeaways

The core implication is simple: many assumptions that shaped internet playbooks for the past 10–30 years are no longer stable. Business models built on those assumptions may become obsolete faster than people expect.

There’s a recurring failure mode in tech transitions: even after a new paradigm arrives, old business models keep growing due to inertia, which leads people to underweight the probability of structural change.

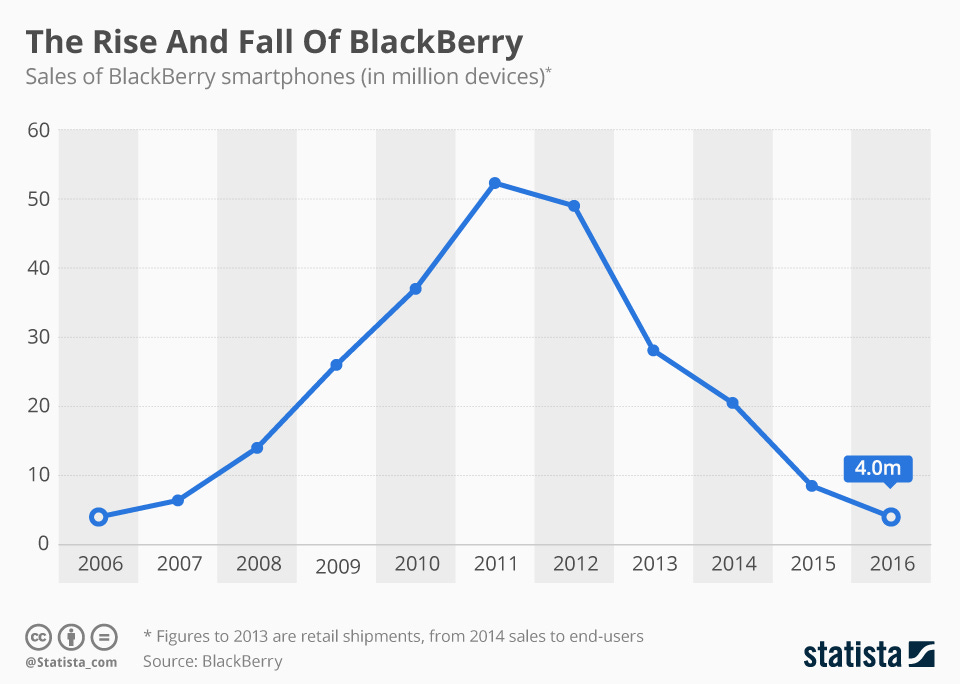

BlackBerry is a clean example. In retrospect, its collapse looks inevitable after the iPhone. But historically, BlackBerry actually grew for years after the iPhone (2008) and App Store (2009). It peaked around 2011—roughly 4x larger than it was in 2008.

The lesson: a business can be growing—strongly—while still moving in the wrong direction relative to the next market structure. And a decade later, it becomes the new BlackBerry.

If you’re building now, don’t be the “BlackBerry” of the Intent Economy.