[Two Cents #83] “Flights of Thought” on Consumer + AI — Part 9: Consumer Behavior Shifts — 1. The Beginning

Restarting, with a different approach

I’ve been trying to map Consumer + AI by walking through individual verticals and listing “potential opportunities” (e.g., education in [Two Cents #81]). I’ve come to believe that’s not the best way to do this.

Founders—not investors—are the ones who discover the real wedge. They live inside the problem long enough to see what outsiders can’t: the hidden constraints, the behavioral friction, the second-order effects. Even when a product looks “obvious” in hindsight (Uber, TikTok, Snapchat), getting to PMF—and then turning early-adopter behavior into mainstream habit—is an exhausting, non-linear craft. It’s hard to appreciate from the outside.

And when a casual observer lays out “the opportunities” too early, it can actually narrow founder imagination. It can keep the conversation shallow, or worse, anchor a team to a premature framing. That’s an easy form of investor arrogance to fall into. I’ve fallen into it before.

So I’m changing the lens: instead of enumerating startups-by-vertical, I want to focus on insights and value props—the kinds of shifts that create new behavior. Let founders own the path from thesis to product.

Going forward, I’ll share a set of “starting points” that might help founders find concrete problems inside Consumer + AI. And when helpful, I’d like to be a thinking partner as they go from macro shift → specific wedge.

Tech shifts trigger consumer behavior shifts

Human needs don’t fundamentally change. But when technology changes the form factor, distribution, and cost structure of how needs are served, behavior changes—slowly, then suddenly. And when behavior changes, business structures eventually follow.

Early automobile history is the canonical example. If you asked consumers what they wanted before cars existed, they might have described “a faster horse.” They couldn’t predict highways, suburbs, logistics networks, road trips, or the re-architecture of cities. The invention wasn’t the story—the second- and third-order consequences were.

AI is that kind of enabling technology.

Where generational companies come from

From a consumer investor’s perspective, generational companies are born where tech shifts intersect with consumer behavior shifts—where a new capability unlocks a new default habit.

Web 1.0 produced Google and Amazon. Mobile produced Uber, WeChat, Coupang. These weren’t just better products; they shaped new behavior at scale.

An early-stage VC’s job is to find these generational opportunities before they’re obvious. Over the last 30 years, examples include Google, Roblox, Facebook, Uber, Tencent (WeChat), ByteDance (TikTok). In Korea: Naver, NCSoft, Nexon, Kakao. In the AI era, the goal is the same: identify the winners early, earn allocation, and help them compound.

Tech shifts vs. behavior shifts: causality usually runs tech → behavior

Tech and behavior influence each other, but in most cases the direction is simple: new tech makes previously impossible things possible, and behavior follows.

Mobile didn’t just improve the internet—it introduced new primitives: location tracking, always-connected usage, a camera in everyone’s pocket. Those primitives enabled new behaviors, and new companies followed (Uber, Instagram, TikTok).

It’s also useful to think in orders of magnitude, not binaries. A 2x improvement often reshapes incumbents. A 100x–1000x improvement creates behaviors that were effectively impossible before.

Generative media is a clean example. When image/video/music creation becomes dramatically cheaper and easier, creation expands from “experts” to “everyone,” and new forms of creativity emerge. At the same time, professionals don’t disappear—they move to a different frontier of craft, just as painters evolved after photography. Photography didn’t kill art; it created a new medium and forced differentiation.

A closer example: when video distribution approached near-zero marginal cost, entertainment shifted from film-and-broadcast constraints to personalized, on-demand streaming. The medium changed; the consumer habit changed.

On the time window of change

These transitions play out over long arcs. Mobile took ~10+ years to fully reshape behavior. The web took ~30 years.

The timeframe depends on how “new” the behavior is. The web’s core shift—democratized information distribution—created fundamentally new social patterns. Mobile, in many ways, was a massive form-factor upgrade on existing behaviors (more continuous, more accessible).

By that framing, AI looks closer to the web than to mobile: it introduces genuinely new capabilities, not just a better interface. A 30–50 year arc seems more realistic than a 5–10 year arc—while acknowledging that the most investable company formation happens in the early chapters of that arc.

So if we want to reason about consumer behavior change, the practical method is:

identify what tech now makes possible that previously wasn’t, and then

model the first-order and second-order behavioral consequences.

That’s the framework I’ll use in this “consumer behavior shifts” series.

Two broad arenas of consumer behavior change

You can over-intellectualize this with Maslow, but a simpler split is useful when evaluating new consumer services—especially if you’re building for a 3–10 year horizon.

1) “Survival” needs: products & services

Products: commerce, logistics, physical goods distribution.

Services: everything else that supports life and productivity—education, work, health, finance, transportation, travel.

If I list early keywords for how AI changes this arena:

white-glove AI concierge, hyper-personalization, lifetime companion, near-zero marginal cost.

If you can translate a combination of these into a crisp value proposition that feels inevitable, you’re usually staring at a real opportunity.

2) “Play” needs: the Spectrum of Play

When tech shifts happen, “play” tends to react first—and monetize first. Entertainment pushes new primitives to their limits.

Historically: adult content seeded early web monetization; then games and broader entertainment followed. If you widen the lens, sports betting and even prediction markets can be seen as extensions of this “play” impulse—though I’m still forming my view on what that implies.

My prior is simple: the play economy remains a huge share of consumer spend and attention, and it will be among the first places AI-native behavior becomes mainstream.

Is this the opening of Consumer + AI?

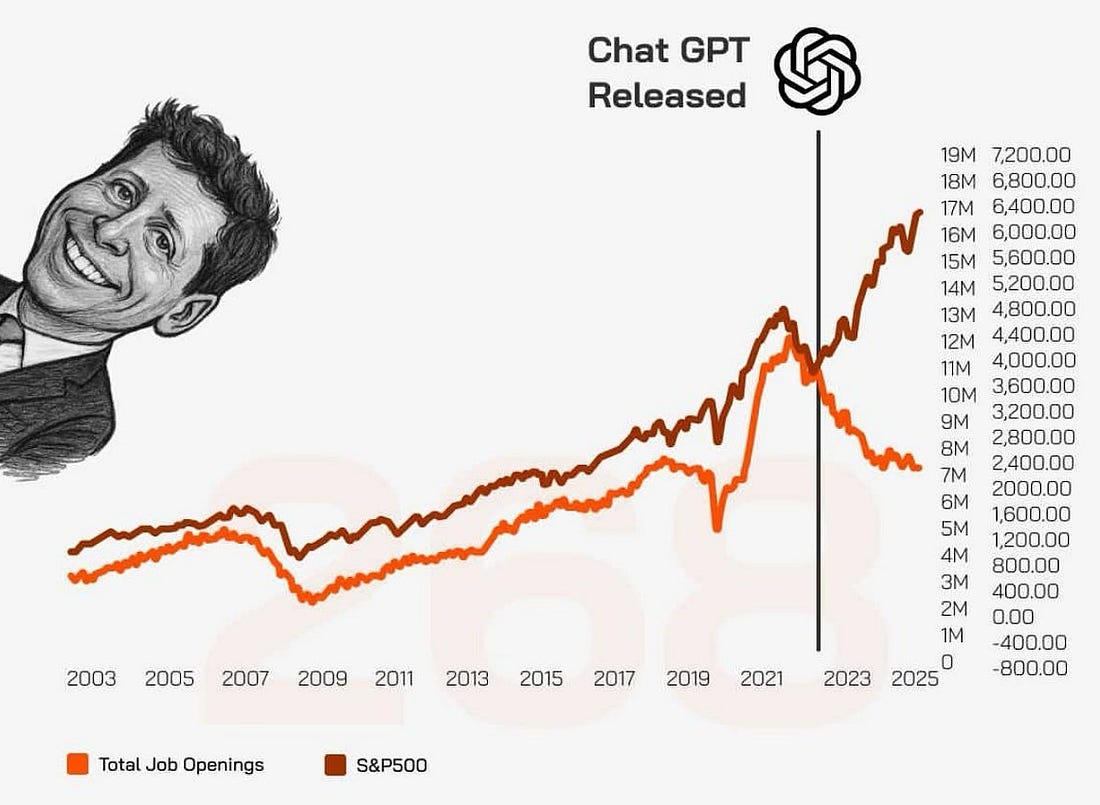

For the last three years, especially in the U.S., the AI industry has been enterprise-first. Consumer experimentation existed (image/video generation, lightweight GPT wrappers, AI companions), but the deeper question—what new consumer behavior AI enables—has only recently started getting serious attention. (In Silicon Valley, I only began hearing “Consumer AI” as a mainstream phrase around 2025 Q3–Q4.)

Why enterprise moved first

Enterprise had the perfect conditions:

immediate willingness to pay for productivity

proven ROI

existing IT budgets that could be reallocated

relatively low price sensitivity versus consumers

When a coding agent can plausibly pay for itself, a $200/month price point isn’t a deal-breaker. That makes token-cost economics less visible to the buyer.

I expect enterprise adoption to stay strong for a long time—expanding steadily, more linear than exponential, because organizations and spending patterns evolve slower than consumer habits.

Why consumer will be slower—but larger

Consumer scale requires behavior change. That means:

the value proposition must feel personally obvious

new habits must form

many products need a critical mass before the flywheel kicks in

In prior cycles, abundant VC liquidity helped companies bridge the gap from “new tech” to “new habit.” This time, the macro environment is different, and token costs can become a real constraint in price-sensitive consumer markets.

However, AI also has one major advantage versus prior cycles: the distribution substrate already exists. We don’t need broadband penetration (web) or smartphone adoption (mobile) as a precondition. The initial critical mass is already here—though the dominant form factor and UX may look very different 10 years from now.

Net: consumer may take longer to re-architect, but the upside is larger if you become the default surface—an “AI-era Google”-scale outcome.

And as a separate point: Korea has historically been unusually strong at inventing new consumer behaviors during platform transitions (Cyworld-era social, Lineage-era gaming, etc.). That creative edge can matter disproportionately in consumer.

Tech keywords that could trigger new consumer behavior

At this stage, a few “trigger” themes stand out:

Near-zero marginal cost content generation → the “YouTube-ification of everything”

Lifelong personalization with infinite options (personalization as a compounding asset)

Entertainment gets re-imagined end-to-end

Agents as a new Consumer OS

Rebuilding online social infrastructure: ads, discovery, connection—what we used to call marketplaces

I’ll unpack these as first-order and second-order effects, and connect them to startup opportunity spaces.

These triggers will also interact with broader consumer environment shifts—demographics, labor disruption, geopolitics, and the macro shift away from abundant cheap capital. The causality is rarely one-way; it’s a dynamic system.

A second lens: consumer environment changes

Some investors anchor more heavily on macro and social data—demographics, wealth transfer, job market turbulence, de-globalization, and capital cycles—then infer what consumers will do next.

That’s a valid approach, and there are great data-driven references (e.g., government social trend reports, or investor research like Digital Native’s chart-based analysis).

In Two Cents, I’ll take a slightly different stance: I’ll focus less on describing what’s already happening, and more on what AI changes in the environment itself—and what behaviors that newly enables.

What comes next

From here, I’ll go keyword by keyword—what it means, what consumer behavior it could unlock (first-order and second-order), and what kinds of startups could emerge.

This won’t be a 10–20 year grand forecast. It’s a snapshot meant to be useful for founders building now, centered on what may plausibly shift over the next 1–3 years—the window where new behaviors start to form and early category winners begin to appear.