[Two Cents #79] “Flights of Thought” on Consumer + AI — Part 5: Commerce — 1. Agentic Commerce

Introduction

It’s becoming clear that the market’s “readiness” for Consumer AI has crossed a tipping point.

What we need now is to get far more concrete about how AI-driven market change will unfold—the direction, the mechanisms, and the implications for industry structure, competitive dynamics, and the economics between participants.

For founders, the job is to identify those opportunities a little earlier and move first. For investors, the job is to recognize those early moves quickly and support them aggressively.

This series—my “Flights of Thought”—is an attempt to share how I’m thinking through what will happen, what it will unlock, and what kinds of ideas are likely to matter.

Now it’s time to move from macro themes to concrete opportunity spaces by vertical.

I’ll start with commerce, because it’s arguably the clearest category to model—at least on paper. (That confidence may prove wrong, but it’s a good place to begin.)

Commerce + AI as a new “frontier”

The most important premise: most sellable products are already online. There are still offline pockets, but they likely won’t be the decisive part of the market.

That matters because the AI-driven transformation in commerce is unlikely to be “a new wave of products going online.” It’s not primarily a new Amazon/Coupang—i.e., a new product-page database.

The real battlefield is access and distribution: who controls how consumers discover, select, and buy products that are already digitized and purchasable.

Under that premise, the first major shift is obvious: today’s purchase journey—

Google search → product page (Amazon/Shopify/etc.) → browse/compare → checkout—

will compress into agent-led, increasingly autonomous flows.

In other words: Agentic Commerce moves from concept to default.

Structural shifts driven by Agentic Commerce

The core change is not “better tech.” It’s a change in the actor: the buyer becomes an agent.

Consumers won’t browse individual stores, compare products, and check out manually. They’ll delegate.

“Keep my weekly grocery spend under $100 and restock what I need.”

The agent executes the plan and returns an outcome—either fully purchased, or pre-filled carts waiting for final confirmation.

Once agents own discovery → selection → checkout, the economics of the entire stack shifts:

Search (SEO / ads)

Commerce platforms

Payments

Retargeting, cart ads, affiliate loops

Merchant tooling and attribution

In the old world, intent flowed from search → ads → product discovery → checkout via payment processors. In the agent world, intent is captured once—then the agent executes end-to-end.

That means value gets redistributed. Some incumbents lose leverage. New intermediaries appear. Gross margin pools move.

That is where startups get paid.

Early on, we’ll see demand- or vertical-specific agents that lock in user habits. The winners can expand into broader platforms. And we’ll need new infrastructure “rails” to make any of this work: product data access, multi-merchant aggregation, automated checkout, and persistent shopping memory/personalization.

Incumbents are already taking different positions

Even today, large commerce players are reacting very differently—because each one is defending a different moat.

Amazon is effectively trying to restrict external agent access to its product data—its most strategic asset—while building its own agent layer (“Shop for Me”-style direction). The goal is simple: keep the consumer surface, block the disintermediation.

Shopify is more nuanced: allow product discovery, but restrict checkout. That’s consistent with Shopify’s incentives—payments and fintech economics are central. Open the top of funnel to developers, keep the bottom of funnel in-house.

Walmart has been comparatively more open: allow access, let agents drive traffic and sales. That can be rational if you believe openness increases volume—or if you’re fighting from a less dominant position and can’t afford to shut off new distribution.

This divergence creates whitespace. As SEO and search ads lose leverage, the premium shifts to:

agent-friendly APIs

multi-merchant data layers

automated checkout rails

identity, permissions, and trust primitives

personalization/memory systems

How the consumer purchase journey changes by category

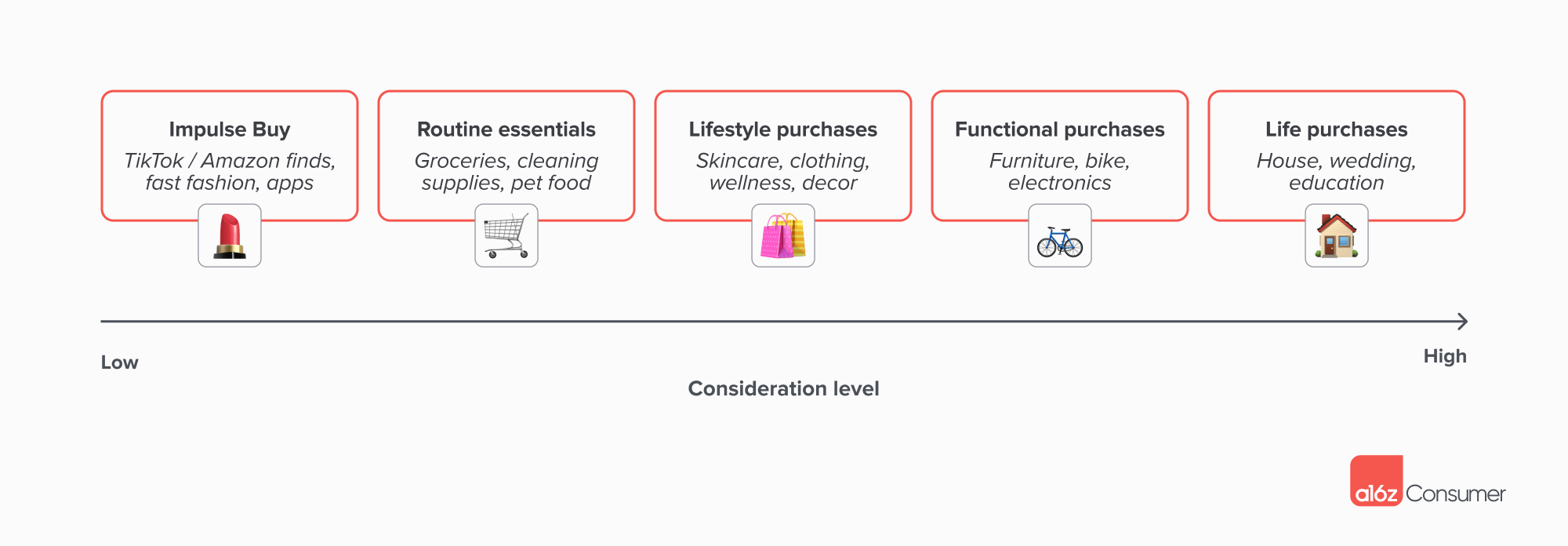

As a16z has framed it, consumer purchases can be grouped into five broad types—each with different decision dynamics. In an AI-native commerce world, each will evolve differently:

Impulse purchases

From checkout-line candy → TikTok/Instagram “buy in 5 seconds.”

AI’s role is less “research” and more “conversion + friction removal.”

Routine essentials

Detergent, toilet paper, pet food → agent-managed replenishment.

Not subscription-by-calendar, but replenishment-by-state: the agent infers when you’ll run out.

Lifestyle purchases

Beauty, fashion, home—highly taste-driven.

Requires a persistent personalization layer that tracks your history, your preferences, and the market’s shifting trends. This may naturally become an ambient agent behavior.

Functional high-consideration purchases

Laptop, bike, sofa.

The agent becomes a research analyst and procurement advisor: market scan, shortlist, trade-off explanation, and negotiation—often with a brand-side agent on the other end.

Life purchases

Home, car, wedding, college—large, multi-step decisions.

This starts to look like a “butler agent”: research, staged consultation with you, coordination, and even financing solutions.

The implication is straightforward: agentic commerce is not one product category. It is five different problems, with five different UX and monetization shapes—hence five different startup opportunity maps.

What “fully autonomous agentic shopping” can look like

Given those different journeys, autonomous shopping will likely emerge in multiple structures:

1) Personal agents (consumer-facing)

Automate repeat demand end-to-end.

Example: “Under $120/week, restock groceries aligned with my diet.”

Monetization could come from subscriptions, affiliate economics, and recommendation-driven upsells.

2) Category-specific agents

Specialists for high-consideration categories (electronics, travel, furniture).

Beyond checkout automation: research, negotiation, warranties, and human-in-the-loop moments—delivered as a new buying workflow.

This is where startups can own a vertical wedge early—until horizontal platforms (Amazon, ChatGPT-level super-apps) attempt to absorb the behavior.

3) Enterprise / brand agents

Brands and retailers will increasingly put forward their own agents as the frontline sales rep.

These agents will upsell, cross-sell, and personalize in real time. That creates a clear “agent-as-a-service” SaaS opportunity for merchants—structurally similar to the way Klaviyo/Attentive rode the marketing automation wave, except the agent becomes the primary interface, not just the automation layer.

4) Marketplace / platform agents

A more integrated model: a platform agent that coordinates across sellers and brand agents to deliver the entire journey.

Here the AI dynamically composes bundles across SKUs, merchants, budgets, and constraints—effectively acting as a concierge that “just handles it.” At that point, the distinction between “agent” and “platform” starts to blur.

Unlike Amazon/Google’s centralized model, an AI-native aggregator—or a network of brand agents that represent supply—could evolve into a new kind of marketplace.

Startup opportunities that fall out of this shift

These are early sketches—examples of what becomes possible if the structure shifts the way we expect. The real opportunity set will expand as the market evolves.

1) Infrastructure (agent “picks & shovels”)

The deepest opportunities are often the rails.

To enable agents to transact, commerce needs new primitives: data access, negotiation, identity, checkout, memory. Whoever builds these layers becomes foundational.

Examples:

Multi-merchant aggregation APIs / agents

Connect to Amazon, Shopify, and long-tail merchants, normalize catalog access, and enable agent-to-agent negotiation. Think “Plaid-like connectivity,” but for commerce inventory and purchasing flows. The exact shape depends on how A2A economies and agentic commerce converge.

Agent-native payments and checkout

M2M payments, delegated checkout, programmable permissions. A large portion likely shifts toward stablecoin-like rails or at least non-human-first assumptions. The mental model is “Stripe for agentic commerce.”

Memory + personalization engines

Persistent shopping constraints and context: “Only vegan under $50,” “auto-reorder staples when my state indicates I’m low,” preferred suppliers, substitution logic. A “Twilio for consumer context”—a layer other apps build on.

These companies can become the rails that the rest of the ecosystem depends on—like Twilio (communications), Plaid (fintech data), and Stripe (payments) did in prior eras.

2) Consumer apps (autonomous shopping agents)

This is the new “search bar.” Whoever owns the delegation interface owns the consumer commerce surface.

Examples:

Personal shopping agents for staples, budget control, price tracking, calendar-aware replenishment.

Cross-platform agents that route across Amazon + Shopify + direct brands—generalizing “Shop for Me” into a multi-platform aggregator.

In past cycles: Honey captured coupons, Instacart captured grocery execution. In this cycle: the winner captures the first consumer touchpoint for buying.

3) Vertical AI shopping agents

The clearest wedge opportunities are verticals where Amazon is weaker and consumers need expert guidance—typically higher-margin, high-consideration categories.

Examples:

Travel agents that bundle flights/lodging/activities with personalization + real-time price tracking

Health & wellness agents that manage OTC/supplements linked to personal health context

Luxury & fashion agents that curate and extend into resale/circular consumption

Financial product agents that optimize cards/insurance/refinancing with continuous monitoring

Historically, Expedia (travel), Oscar (insurance), and Farfetch (luxury) built large businesses through vertical focus. This time, the “expert layer” becomes AI-native and can replace or redefine the UX entirely.

4) Merchant tools / brand agents (agent-as-a-service)

Brands won’t just run Shopify stores. They’ll run AI agents that interact 1:1 with customers.

Examples:

Agent storefronts: conversational, personalized first sales rep

Conversion optimization agents: real-time upsell/cross-sell at checkout

Post-purchase care agents: warranty, support, replenishment, retention

This mirrors prior merchant SaaS stack land-grabs (support, CRM, marketing automation). The difference is that the agent becomes the front door, not just the workflow layer.

Closing

Agentic commerce is not “ecommerce getting smarter.” It’s a restructuring of the commerce value chain.

As search ads, SEO, marketplace ads, and payment models that powered the last 20 years get rewired, large new profit pools open—and new companies will be built to capture them.

Shopping will move from “search → compare → checkout” performed by humans to delegated, increasingly autonomous execution by AI.

Just as mobile transitions produced mobile-native winners (KakaoTalk, Baemin), this transition will produce agent-native winners—and likely the next wave of consumer unicorns.

This is the starting line.

Call for Startups

The purpose of sharing this thinking is straightforward. As an early-stage investor focused on Consumer + AI, I hope this series helps existing startups better leverage AI-driven shifts—and helps new founders reduce trial-and-error as they search for meaningful opportunities.

In that sense, this is Two Cents’ version of a Call for Startups.

If you are an early-stage founder or startup in Consumer + AI and believe you are onto something, my inbox is always open. Feel free to reach out via DM or email:

hur at hanriverpartners dot com